Hydrogen Generation Market Expected to Reach US$ 427.07 Billion at 8.27% CAGR by 2034, │ The Insight Partners

Fuel by Regulatory Measures, Hydrogen Vehicle Industry Growth, and Green Energy Transition

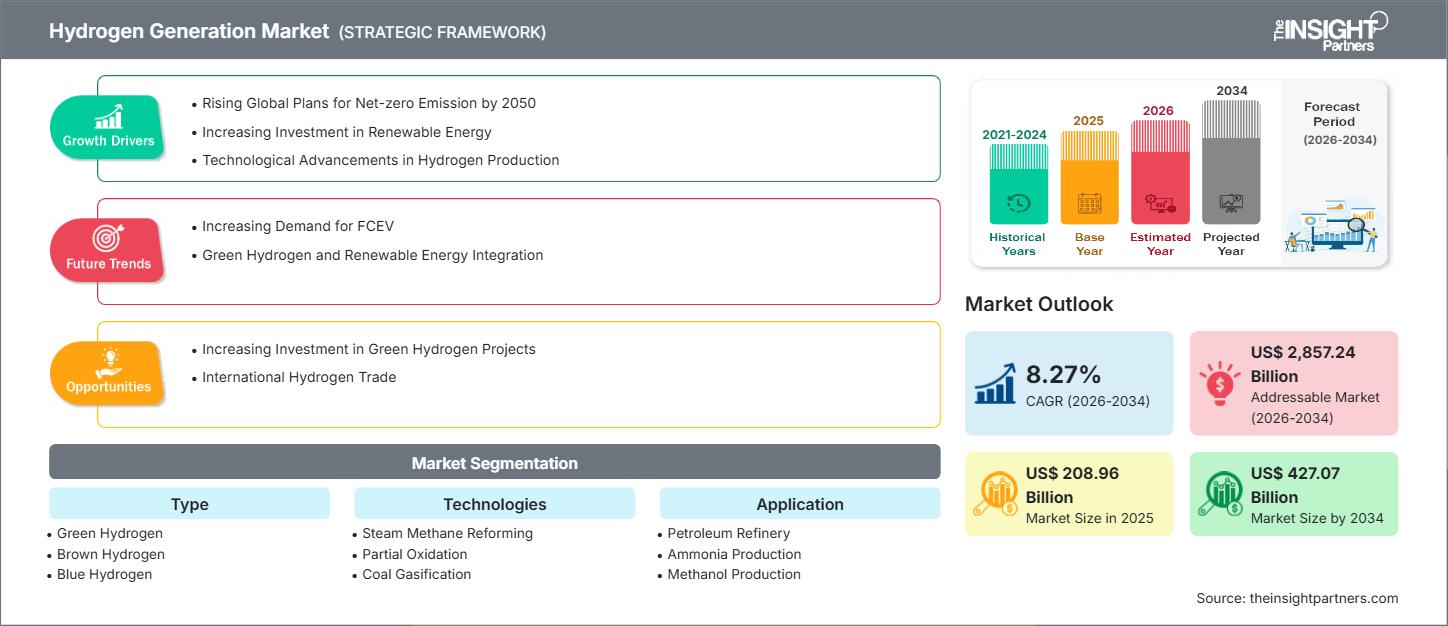

New York, June 23, 2026 (GLOBE NEWSWIRE) -- The Insight Partners, published its latest market intelligence report on the Global Hydrogen Generation Market. The study finds the market, valued at US$ 208.96 billion in 2025, is projected to reach US$ 427.07 billion by 2034, registering a compound annual growth rate (CAGR) of 8.27% over the 2025 - 2034 forecast period. Research draws on primary interviews with C-suite executives, OEM engineers, procurement heads, and policy analysts across more than 15 countries, augmented by proprietary databases and third-party validation.

Market Overview

The Hydrogen Generation market covers the manufacture of hydrogen using different raw materials and conversion methods. Hydrogen acts as a means of energy and also as an industrial raw material. Major uses of hydrogen are in the refinery, chemical, steel, transportation, and power sectors. The market is going through a major change; the proportion of fossil-derived "grey" hydrogen (mostly from steam methane reformation and coal gasification) is decreasing, whereas the shares of low-carbon "blue" and "green" hydrogen are increasing. This is, first and foremost, due to the acceleration of climate policies and the requirements for industrial decarbonization. Three main factors together support the growth in demand: government policy initiatives like the US Inflation Reduction Act and EU Hydrogen Strategy, net-zero commitments by companies that are generating signals for offtake, and a significant influx of capital in the manufacturing of electrolyzers, storage, and pipeline infrastructures. The industrial sector remains the biggest consumer of hydrogen currently, predominantly in refining and ammonia production. However, transport (fuel cell vehicles, shipping, and aviation) and grid-balancing applications are quickly turning into significant growth vectors.

latest research on the Hydrogen Generation Market, covering market size forecasts, growth drivers, regulatory trends, and competitive insights. You may access the Sample document here: https://www.theinsightpartners.com/sample/TIPTE100001037

Key Market Findings

- Regional Leader: Asia Pacific is forecast to account for more than 35% of global market share in 2025, led by China, Japan, South Korea, Australia, and India.

- Europe: Europe holds the second-largest share at over 25%, with the German market projected to grow at a 8.56% CAGR through 2034.

- Dominant Segment: Steam Reforming remains dominant in terms of market share and CAGR (%) from 2025 to 2034.

- Fastest-Growing Application Segment: Ammonia Production Segment to Register the Highest Market Share and the Highest CAGR

Primary Growth Driver: Infrastructure Investment and Urbanization

The primary driving factor fuelling the hydrogen generation market is the rapid global shift towards low-carbon energy systems that are being backed up by stringent government policies, industrial decarbonization targets, and increased demand for clean fuels. Countries from various continents, like Europe, North America, and Asia, are not only establishing hydrogen production targets but also giving incentives and funding large-scale electrolyzer and hydrogen infrastructure projects to reduce their dependency on fossil fuels. Besides that, sectors that are difficult to decarbonize, like refining chemicals, steel and heavy transport, are increasingly looking at hydrogen as a way to lower their emissions while still ensuring the supply of energy. Also, green hydrogen is being embraced as an alternative as renewable energy costs continue to decline and the efficiency of the electrolyzers improves. As a result, clean hydrogen is becoming a viable business option. On top of that, governments and companies are going ahead with their commitments to develop local hydrogen production to cut down on foreign fuel dependency. These developments have led to an ongoing expansion of the industry's total capacity.

Steam Reformer: A High-Value Process Segment

The primary driving factor behind steam methane reforming's market dominance is the increasing global demand for hydrogen across various industrial applications, particularly in ammonia production (39.08% market share), petroleum refining, and emerging clean energy sectors. This demand surge is fueled by hydrogen's role as a clean energy carrier and its critical use in ammonia for fertilizers, methanol production, and oil refining processes.

Get a customized report to align these insights with your strategic business objectives - https://www.theinsightpartners.com/customization/TIPAT100001342

Segment Analysis

Steam Reformer - Market-Leading Process Segment

Steam reformer, specifically steam methane reforming, registered the highest market share in 2025 within the hydrogen generation market. It remains the dominant process because it is the most mature, widely deployed, and cost-efficient production route for large-scale hydrogen output, especially where natural gas is readily available.

This part of the hydrogen market is dominating due to the fact that the existing refinery, ammonia, and chemical plants' networks have been designed around conventional hydrogen production. As a result, steam reforming benefits from a huge existing base of installations and so has lower near-term switching costs. Besides that, for one thing, nowadays a lot of industrial users still trust it for a dependable high-volume supply. Then again, research shows that electrolysis is taking the lead in low-carbon applications.

Formerly, electrolysis was the only way for the clean hydrogen market to evolve that was contemplated by policymakers and corresponded to renewable power integration. It is because of capital costs being high and dependence on power that electrolysis will still have a smaller share compared to steam reforming in 2025. Besides natural gas reforming, coal gasification, together with the other methods, comprises the portions of the market that is much smaller. The main reason for their existence is that, in reality, certain regions have coal-heavy energy systems or industrial demand that requires these methods.

Ammonia Production - Highest Market Share and Fastest-Growing Application Segment

Ammonia production is the largest application segment in the hydrogen generation market, driven by its critical role in fertilizer manufacturing. The process relies on the Haber-Bosch method, which synthesizes ammonia directly from nitrogen (from air) and hydrogen (typically from natural gas via steam reforming) using an iron catalyst under high pressure (200–400 atmospheres) and moderate temperatures (400°–650°C). The production involves six key steps: natural gas desulfurization, catalytic steam reforming, CO shift conversion, CO₂ removal, methanation, and ammonia synthesis. Ammonia is one of the largest-volume synthetic chemicals globally, with fertilizer manufacturing accounting for approximately 70-80% of total ammonia demand.

Chat with us - https://tawk.to/chat/5d56720577aa790be32f2bec/default

Regional Analysis

Asia Pacific - Highest Market Share and Fastest-Growing Market

Asia-Pacific shows the highest market share and growth in the hydrogen generation market, driven by rapid industrial expansion, strong energy demand, and aggressive government support for clean hydrogen infrastructure. The region is benefiting from major investments in electrolyzers, hydrogen hubs, refueling networks, and low-carbon industrial projects across China, Japan, South Korea, and India.

China is playing the largest role in this momentum, with large-scale renewable hydrogen targets and heavy spending on hydrogen infrastructure. At the same time, Japan and South Korea continue to support hydrogen imports, fuel-cell mobility, and industrial decarbonization. India is also emerging quickly through national hydrogen mission initiatives and growing interest in green hydrogen for refining, fertilizers, and mobility.

Compared with North America and Europe, the Asia-Pacific is growing faster because it combines a broad industrial base with rising domestic energy needs and strong policy backing. Europe remains highly active in clean hydrogen deployment, but its growth is more regulated and infrastructure-heavy. North America is also expanding, especially through tax incentives and hydrogen hubs. Still, Asia-Pacific has the widest mix of end-use demand and project scale, which is why it is expected to register the strongest growth rate in the forecast period.

Market Dynamics: Key Opportunities and Challenges

Government Policy Support and Green Hydrogen Mandates Accelerating Electrolyzer Deployment: One such factor driving change in the hydrogen generation market includes the widespread rollout of national policy initiatives, driven primarily by state governments and backed by strict green hydrogen quotas. The number of nations developing hydrogen strategies already exceeds 30 countries worldwide, which have pledged a combined total investment of over $300 billion through 2030 towards the development of this nascent sector.

In the U.S., the newly passed Inflation Reduction Act will provide a production tax credit of up to $3/kg for green hydrogen generated using low-carbon electricity. This single incentive program alone has resulted in over 100 GW of green hydrogen generation capacity being announced by electrolyzer operators in North America in just a few months. The European Union, meanwhile, has mandated 10 million tons of locally produced hydrogen using renewables by 2030 as part of its REPowerEU program, triggering the Hydrogen Bank auction process that awarded €800 million in incentives for green hydrogen projects in its inaugural auction.

Industrial Decarbonization of Hard-to-Abate Sectors Unlocking Massive Green Hydrogen Demand: One of the most important and significant opportunities in the hydrogen production market is the deep decarbonization of difficult-to-decarbonize industrial sectors such as steel, ammonia, cement, and refining that have limited potential to decarbonize through electrification. Combined, these industries emit around 22% of the world’s greenhouse gases, and only through green hydrogen can a nearly zero-production footprint be achieved.

An example of this sector is steel production, where blast furnace steelmaking depends on metallurgical coal as a reductant, generating 1.8 tons of CO₂ for each ton of steel produced. In hydrogen-based direct reduction, pioneered by HYBRIT in Sweden and H2 Green Steel, metallurgical coal is replaced with green hydrogen, reducing emissions by up to 95%. Since worldwide steel production exceeds 1.9 billion tons annually, any shift from traditional technologies will require the production of many tens of terawatt-hours of electricity from renewables and many millions of tons of hydrogen, which will become a huge boost to the deployment of electrolyzers.

The ammonia and fertilizer industries represent a short-term target, apart from hydrogen being a main raw material: about 55% of the world's hydrogen use is for making ammonia. With this changeover, using green hydrogen for this fixed demand that has been traditionally met with grey hydrogen (made from steam methane reforming) calls for increasing the capacity of electrolyzers at the existing plants, mostly a brownfield method with an already set up infrastructure. Companies like Yara, BASF, and CF Industries are experimenting with green ammonia production, and the marine industry's demand for ammonia as a zero-carbon fuel is getting more and more layers of demand.

Cement making and other high-temperature industrial processes cover a residential market. With carbon border adjustment mechanisms - e.g., the EU CBAM, which starts in 2026 - charging imports for the carbon embedded in them, industrial buyers in export-oriented countries will have strong incentives to switch to green hydrogen if they want to keep their edge. This regulatory-trade combination flips green hydrogen from being a mere environmental choice to a real commercial must, producing a firm, price-inelastic demand that can form the main basis for the long-term global supply of hydrogen projects, anywhere in the world.

Purchase the full report from The Insight Partners upto 40% Discounted Price - Hydrogen Generation Market

https://www.theinsightpartners.com/buy/TIPTE100001037/

Recent Industry Developments (2025 - 2026)

OMV Started Construction of the largest electrolysis plants for green hydrogen in Europe.

In September 2025, OMV is setting another milestone on the road toward a climate-neutral energy future by laying the foundation stone for one of the largest electrolysis plants for green hydrogen in Europe. The 140 MW plant in Bruck an der Leitha is scheduled to go into operation at the end of 2027. OMV will produce up to 23,000 tons of hydrogen annually in the future using renewable energy from wind, solar, and hydropower, making a significant contribution toward reducing the company’s carbon emissions.

Air Liquide invested in the Construction of ELYgator, a 200 MW electrolyzer project.

In July 2025, Air Liquide takes a major step forward in European decarbonization efforts with the final investment decision to launch the construction of ELYgator, a 200 MW electrolyzer project in Maasvlakte, in the Port of Rotterdam. This project reinforces our leadership in low-carbon hydrogen production and represents a significant advancement in the decarbonization of European industrial needs.

Leading Hydrogen Generation Companies

| Company | Profile |

| Linde PLC | Global industrial gas leader and one of the largest hydrogen producers and suppliers worldwide; operates extensive hydrogen production facilities, piping networks, and merchant hydrogen delivery infrastructure across multiple continents. |

| Air Liquide | Major industrial gases company with comprehensive hydrogen offerings across captive and merchant markets; leading in hydrogen liquefaction and purification technologies for industrial and mobility applications |

| ENGIE SA | Global energy company expanding hydrogen portfolio through green hydrogen projects and renewable energy integration; active in hydrogen production, storage, and distribution for industrial decarbonization. |

| Shell Plc | Integrated energy major investing heavily in hydrogen generation across blue and green pathways; developing large-scale hydrogen hubs and renewable hydrogen production facilities globally |

| Plug Power | Leading provider of hydrogen fuel cell systems and green hydrogen production solutions; building an end-to-end hydrogen ecosystem including electrolyzers, refueling stations, and fuel cell power systems |

| Air Products and Chemicals, Inc. | World's largest pure-play hydrogen company with extensive global production capacity; major supplier to refineries, ammonia plants, and metal processing industries with captive and merchant hydrogen |

| Enapter | Innovative company specializing in AEM electrolysis technology for decentralized green hydrogen production; offering modular electrolyzers for small-scale on-site hydrogen generation |

| Orsted A/S | Global renewable energy leader pivoting to green hydrogen through offshore wind-powered electrolysis projects; developing large-scale renewable hydrogen production integrated with wind farms |

| H2Pro | Israel-based technology company developing innovative water-splitting technology for efficient green hydrogen production; focused on electrochemical hydrogen generation with high efficiency. |

| Bloom Energy | Fuel cell company producing hydrogen through solid oxide electrolysis systems, offering on-site clean hydrogen generation for commercial and industrial applications using electricity. |

| Iwatani Corporation | Japanese industrial gas company with significant hydrogen production and distribution network; active in hydrogen supply for fuel cell vehicles and industrial applications across Asia |

| Messer Group | Leading European industrial gases company with extensive hydrogen production and delivery capabilities, serving automotive, chemical, and metal industries with captive and merchant hydrogen |

About The Insight Partners

The Insight Partners is a globally recognized market research and management consulting firm specializing in technology, media, telecommunications, healthcare, and industrial sectors. Research methodology integrates primary data collection, including executive interviews, OEM surveys, and channel partner analyses, with proprietary secondary research databases and econometric modeling. Reports are used by Fortune 500 companies, private equity firms, government agencies, and institutional investors to inform strategic planning, M&A, and capital allocation decisions. The firm maintains research coverage across 50+ industries and 100+ countries.

Report Link: https://www.theinsightpartners.com/reports/hydrogen-generation-market

Request for a free demo of The Insight Partners’ Hydrogen Generation Market & Intelligence Platform

Media Contact: The Insight Partners | sales@theinsightpartners.com | www.theinsightpartners.com

Also Available in : Korean | German | Japanese | French |Chinese | Italian | Spanish

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.